Hopefully you’ve all downloaded your 2015 Soon-to-be Debt Free workbook by now. If you haven’t don’t fret we are only 13 days into the new year, and today is the perfect day to get started!

Today I am going to walk you through all of the pages to make sure you understand how they are intended to be used.

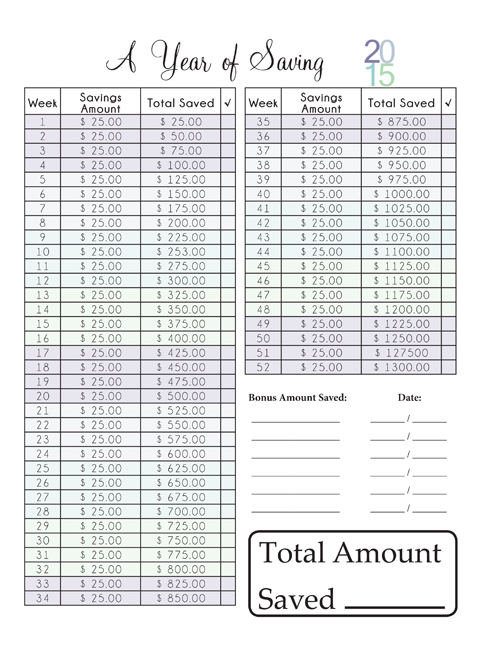

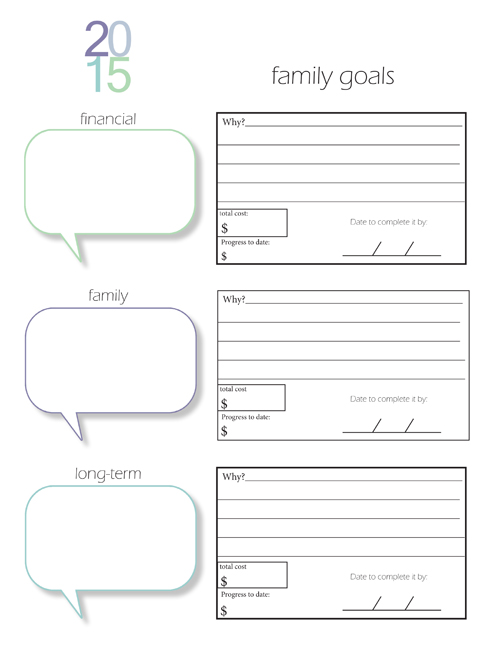

{ A Year of Saving }

If you were to put $25.00 a week into a savings account by the end of the year you’d have $1,300! How nice would it be to have an additional $1,300 in an account to use for Christmas, or new tires on your car, or just to have for when those unexpected expenses arise? There are also lines underneath the chart for you to add additional deposits. Birthday money, did someone give you a lottery ticket and you won a little bit of cash? Save it!

**Please note- if you have at least $1,000 in an emergency fund and other Debts (besides your mortgage) I suggest you put any additional money towards paying down those debts, versus saving it for the unexpected!

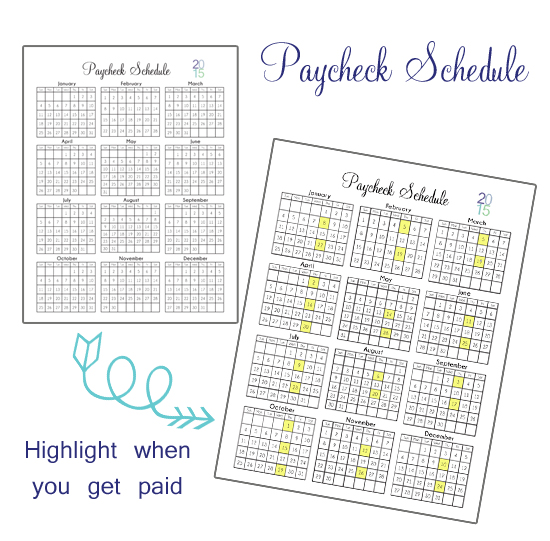

{ Paycheck Schedule }

Go through and highlight the dates you know you’ll be receiving your paycheck! This is a nice reference of when you get paid, and also the weeks you’ll need to pay your bills – based on the paycheck budgeting / bill payment system.

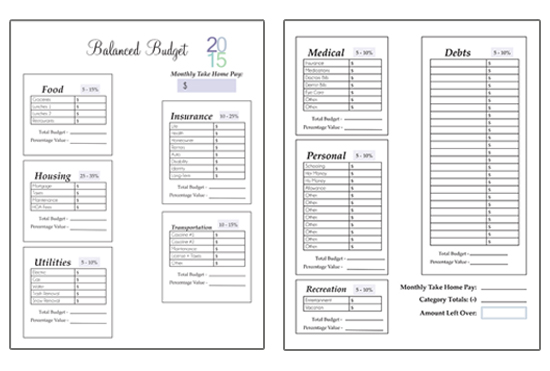

{ Balanced Budget }

These two forms are meant to start you on setting up a balanced Budget. A few things:

- You monthly take home pay needs to be MORE than the total of your categories

- The percentages to the left of each category title show how much of your take home pay the whole category should consume

- The amount left over should be put toward your debts. *See the snowball calculator*

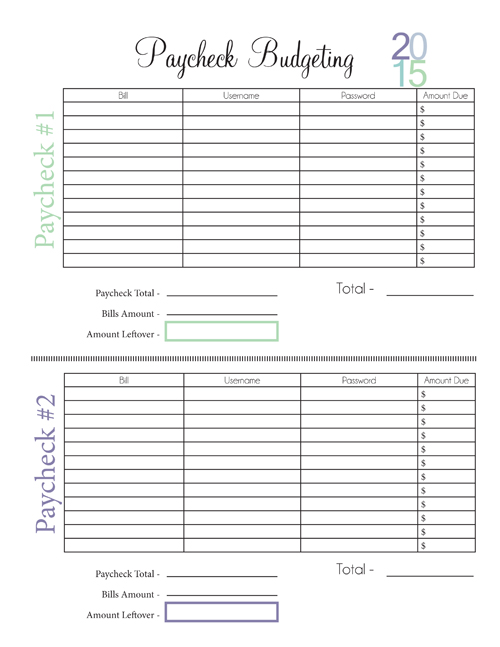

{ Paycheck Budgeting }

This is my method to paying our bills. Scott gets paid twice a month. Guaranteed. So I divided our bills into Paycheck 1 and Paycheck 2 categories. I know that with the first paycheck of the month “these”bills get paid. and “These” bills are paid with the second paycheck of the month.

- You might have to contact a few companies to change your due dates. I have Paycheck #1 bills all due on the 15th or later in the month. (Scott is guaranteed to have a paycheck by the 15th of each month). That way we never ever have a late payment.

- The second paycheck bills are set to be due on the 28h of the month.

Bonus- since he is paid every other week, there are two months in the year that he gets a third paycheck for that month. We consider them bonus paychecks. This year? They will be put toward our student loan debts. That is a pretty great chunk of change to apply towards them.

{ Payment Tracker }

![]()

This form is used to make sure you’ve paid all of your bills for the month. Some things to note:

- For the Due Date – if you use the paycheck budgeting method, I list the date as either P1 (paycheck 1) or P2 (Paycheck 2)

- Because I use my Bill Pay Worksheet – I do not put a check mark in the appropriate box UNTIL the payment has cleared my account.

- I started doing it this way because of our car payment. There is always this little check box I have to click for my payment to go through… it is on the last page – but it always seems like the confirmation page to me. This makes sure I actually pay our car payment on time.

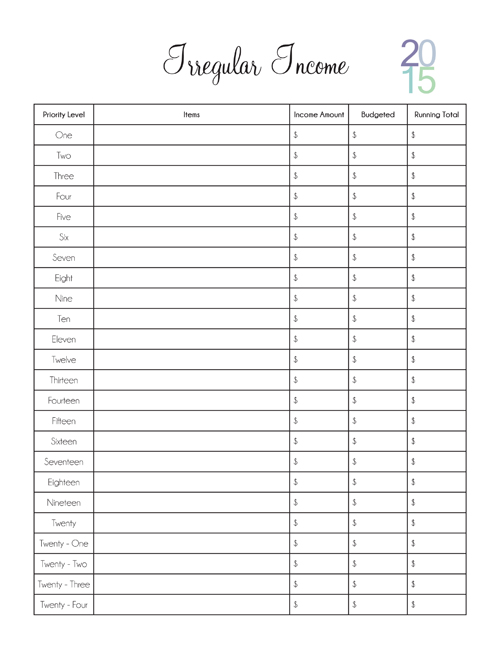

{Irregular Income }

The Irregular Income form is one of my favorites. Simply because it is how I will be helping to provide for the family / pay off our debts. I make a very small income from this little ‘ol blog. When I say very small, I mean very small. However, I hope someday I will be able to remove the “very” from that statement, and then hopefully, god willing I will be able to remove “small” from that sentence as well.

How it works:

- Scott and I sit down and make a priority list of items / debts we want to tackle.

- This list can be any sort of thing. Do you know you’ll need tires for your car next season? Would you love to splurge on a special gift for someone in your family? list it in order of priority on this form.

- I am scattering debt payment amounts in this list. For example: Priority #3 is to put an additional 1,000 on car payment.

- Hop on over to the Budgeted column, and go down the list and write how much you need for each item

- When you get an “Irregular Income” Put that amount in the Income Amount column and go as far down the list as possible based on the income. IE.

- Budgeted Items:

- Priority #1: New tires – $400

- Priority #2: Car Payment Extra – $1,000

- Priority #3: Trip to the Fair – $150

- You received $1,500 in Irregular Income. You’d be able to fully fund the New tires column, as well as the Extra Car Payment and $100 of the Fair Item. So, when the next Irregular Income comes in, you’d pick right up on Priority # 3 (Trip the the fair) until that is fully funded, and then continue down the list.

Now we are going to get into the Debt Repayment Forms! Wahoo!

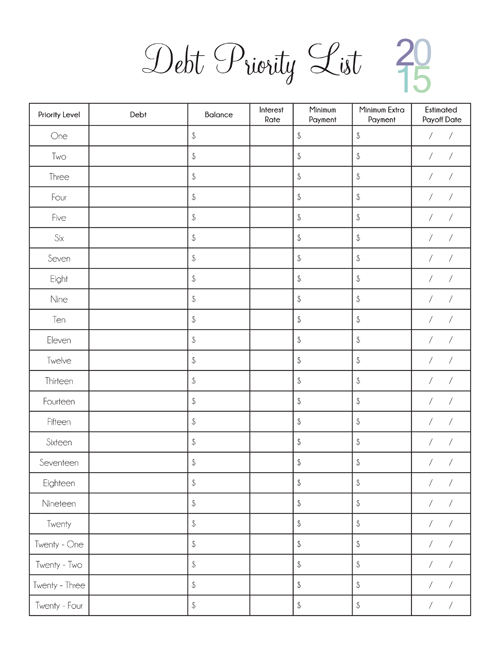

{ Debt Priority List }

On a blank piece of paper list all of your Debts, along with their total balance! *don’t get sick! You can do this!

Once you have them listed determine your debt payoff priority and get to listing them on this form. Make sure you take the time to locate the Interest Rate, and your minimum payments.

- You can go to crown.org and input all of your debt information to determine your Estimated Payoff Date

- Most people recommend you paying your debt off from SMALLEST BALANCE to the LARGEST BALANCE. So you’ll get some “wins” under your belt quickly to keep up the momentum.

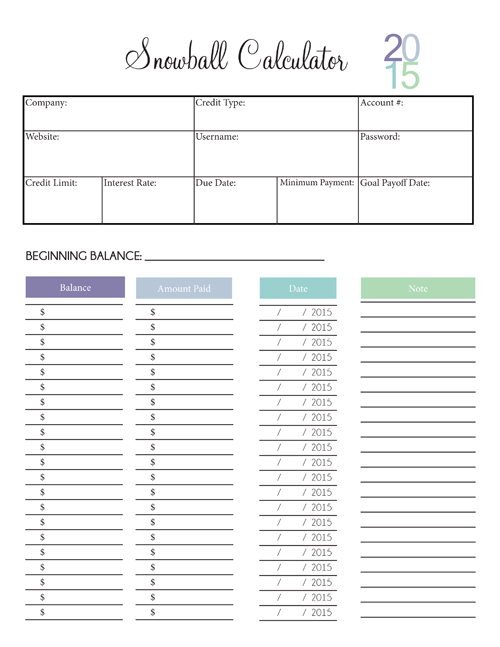

{ Debt Snowball }

Once you have your Debt Priority List figured out, put your use the above form to list your #1 priority. Use this form to track your payments, and watch that balance decrease! I find this form very motivating, as the balance goes down with every payment.

So, how do you and your spouse stick to this all year long, and stay on the same page? Easy, use the following two forms!

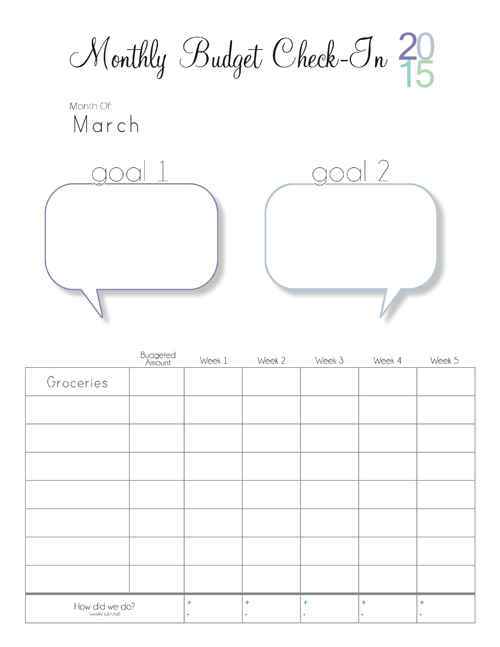

{ Monthly Budget Check-In }

Visit my Month to Month Budget Tracker to get a full rundown on how to use these two forms!

Phew! We made it!

Thank you for all you give us free . I am so thankful for the small thing have a blessed day.

Thank you so much for providing all this for free. You’ve helped me avoid disaster in my young life. I now realize how careful I need to be with my money. You are a saint!

Thank you so much for the printables and I am very eager to get my family on a successful budget. I just have one question. I have noticed on the Balanced Budget sheets that Phone and Cable are not listed on that, would those go under Utilities?

Thank you for providing the forms for free. How gracious of you. I like your forms because there is not a lot of color in them, using more ink. 🙂

Thanks again!

Hi Lindsay,

I just printed your workbook and feel like this will really help simplify things and help my husband understand how I allocate funds every paycheck.

Are you going to be loading a 2016 workbook? I’m just planning ahead since I’m starting in the middle of the year.

Thanks so much for providing them as a freebie!!!!

I absolutely love this! We started this process last month, and by the end of this month, we’ve paid off two of our smaller debts! When will the Soon To Be Debt Free for 2016 be ready??? 🙂

And… I just saw you already responded. 😛 Keep us updated! I’m so psyched about it that I want to be ahead as well!! 🙂

Hi we’re really trying to get out of our debt and start budgeting journaling and planning and saving money for our finances and our financial future.

Hi we’re trying to pay off all debt and get current. With all of our bills. And and start paying off all forms of debt.