Before I get to the good stuff in this post, I just want to take a minute to thank all of you so much! I released the 2017 Financial Planner last week – and the heart felt messages of gratitude, excitement, and praise that I have received – was exactly what I needed to get me through the crash of the site just hours after posting about the release! Truly, thank you all so much!

Okay, now onto the good stuff!

I want to walk you all through the financial planner. I have added some new pages – that deserve an explanation, plus if you are new here, you’ll want to get in on all the goodies! If you have not grabbed your Financial planner yet, you can get it here!

So lets get right into it!

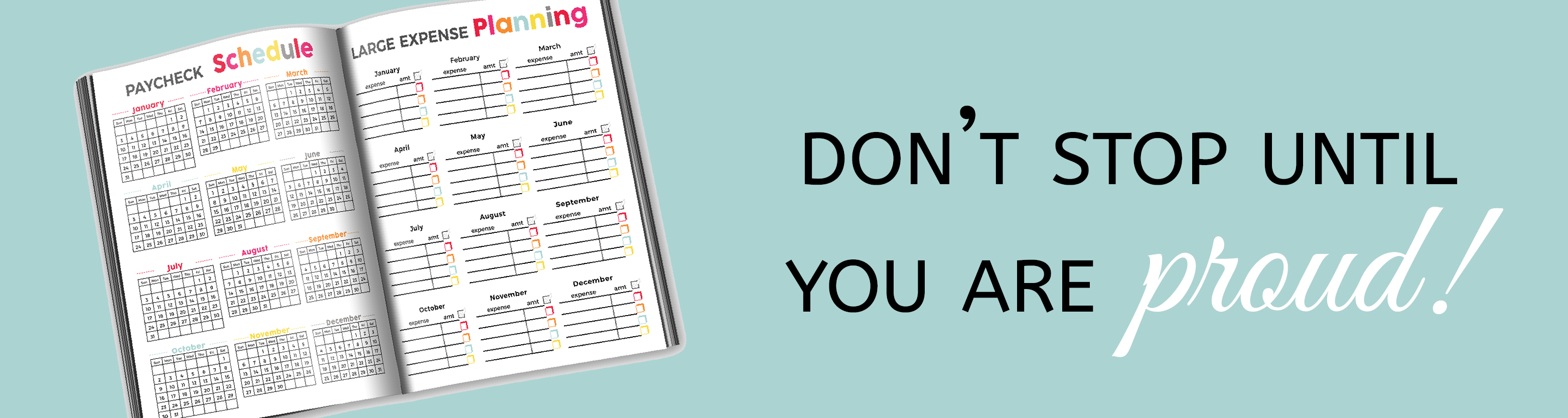

Paycheck Schedule:

Go through this page and highlight (I love these highlighters) the days you get paid. For those of you that get paid every other week – you’ll have two months every year that you’ll receive three paychecks. Make the most of those!

Large Expense Planning:

Stop being blindsided by large expenses – that you should have planned for. Things like the holidays (They do come every year) birthdays, weddings, family reunions. Only you will be able to know if these expenses are worth it to you and your family, while you are trying to get out of debt! Just don’t be impulsive!

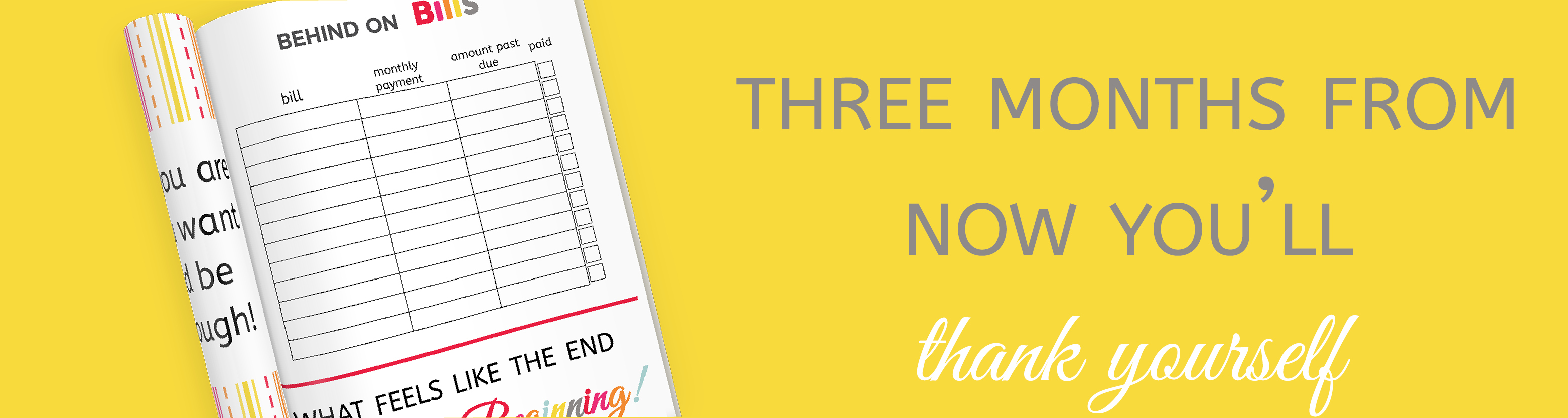

Behind On Bills:

If you are behind on any of your monthly bill payments – or have any money due that you are behind on list them out here. This should be a top priority for you! You need to get caught up before you can get ahead!

Balanced Budget

These two sheets might be the most important! Don’t put in the values that you think they should be – be honest! If you think you should spend only 200 a month on gas, but KNOW that you always spend $275, write that number down. Otherwise, you will never ever stay on budget.

That being said – you also should be stretching yourself and your family to find ways to save money and reduce expenses!

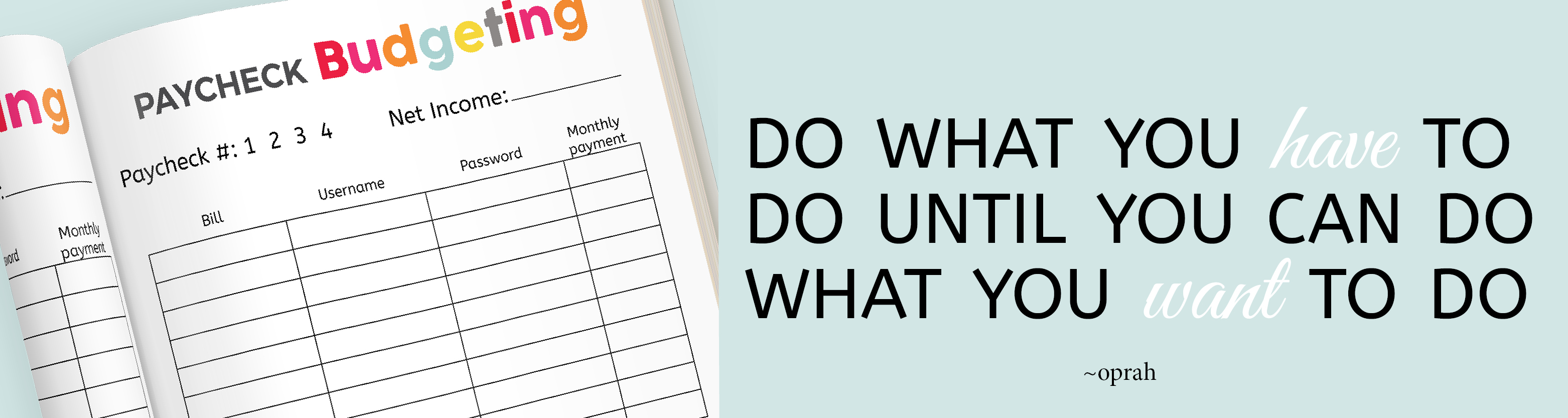

Paycheck Budgeting

When I started paying our bills on the “Paycheck Schedule” everything changed for me. We never miss a payment – it was easy to setup and organize, and easy to maintain! It made it so we never over spend at the beginning of the month just to find out we don’t have enough to cover all our expenses, once I get around to paying them towards the end of the month.

Here is how it works:

- Circle the number that corresponds with the paycheck you are referencing (Is the the first paycheck of the month, the second, third or fourth)

- How much do you Net, for that paycheck (Bring home)

- What bills will you pay out of that sum of money?

- Decide on this, call your bill companies and make sure that their due dates are all AFTER your (1st, 2nd, 3rd, or 4th) paycheck.

- When you get paid, pay those bills!

- Decide in advance how much out of each paycheck will go to: groceries, debt snowball, savings, other

- Write down the percentage values of these amounts. It is nice to see how much (percentage) wise you are spending on your categories each paycheck

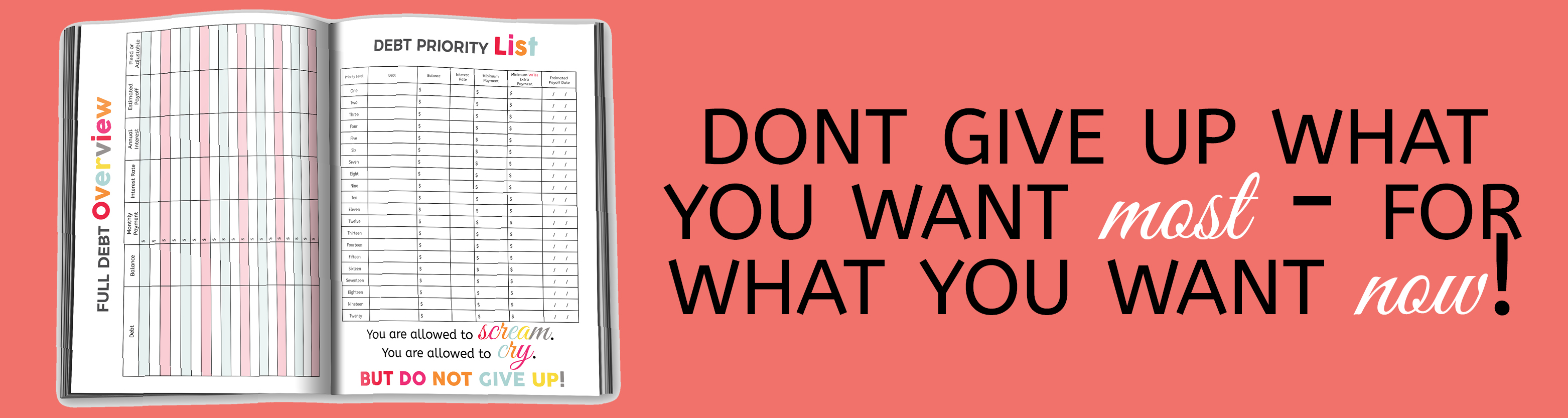

Full Debt Overview

This can be a tough one for people – because some do not want to know the true state of their finances – but let me tell you we all need to know. Don’t be uninformed when it comes to your own life! Write down every debt that you have – and all the information you can about it. What consists as a debt? Any amount or sum that you can “payoff” so your water bill (as long as it is current) is not considered to be a “debt” however things like a credit card, mortgage, student loan, car payment, etc, are debts.

Debt Priority List

Once you have filled out your full debt overview – lets break it down into sizes that seem more manageable. What debts do you want to pay of firsts? List them out in pay off priority. This is the list you will work your way down – paying off the debts one at a time.

Yearly Goals

I want you to set some concrete financial goals for yourself. Some of you might be able to buckle down and get rid of all your debt in 2017. There are some of us, where that would be impossible (Thanks a lot student loans) But that does not mean we shouldn’t have some serious goals that stretch ourselves!

Here is an example:

Goal #1 – pay off the remainder of your car loan that is $5,000. Divide that goal number (5,000) in this example by four (4). Those are your goal increments. As you work towards your goal color in the squares as your reach your increments.

Saving Tracker

Yes, paying off debt is the ultimate goal – but you also need to plan for today and tomorrow. Life is bound to happen – cars are bound to breakdown, and unexpected co-pays come up. If you have no savings to cushion the blows, you’ll continue accumulating debt. Track your savings deposits here.

Irregular Income Tracker

I’ve talked before about how important it is to have more than just one income source (Especially when you are paying off debt). This is where you track your “side hustles” It is important to make sure that money works hard for you. It should not be “fun” money at this point. Don’t blow it!

Irregular Income

This sheet tracks what you DO with your irregular income. The previous sheet tracks how much you make – this sheet tells you how to “spend” it. You should be referencing your Full Debt Overview sheet and your Large Expense Tracker as you fill this sheet out. Work your way down the page. The more you make – the more you get to cross off!

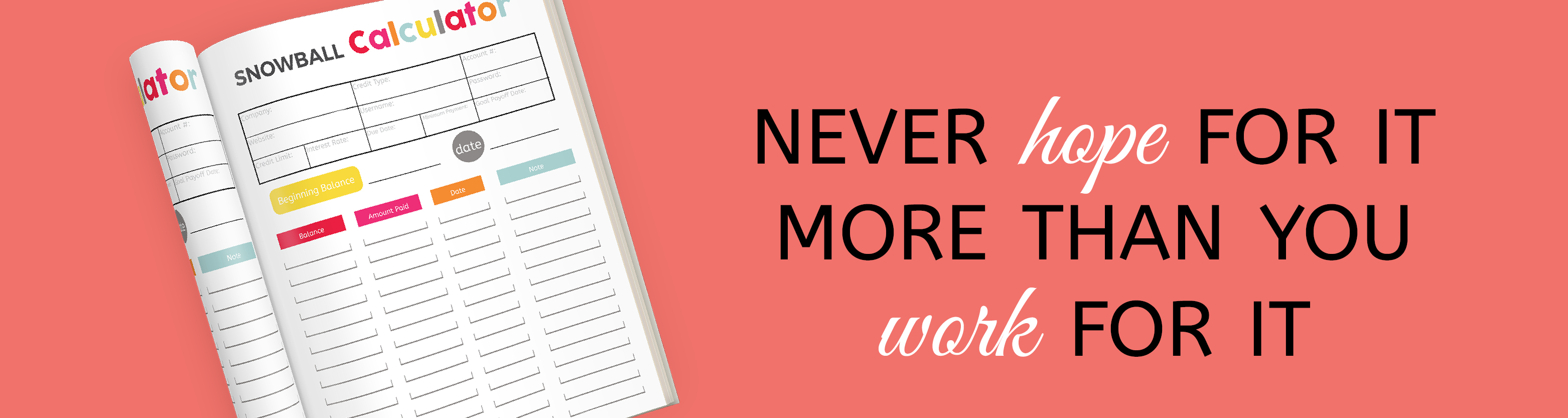

Snowball Calculator

You know what debts you want to knock out first (Because you filled out the full debt overview, right!?) Now – pick the first three on the list, and fill out your snowball calculators. Starting with #1 – pay your minimum balance every month, and every single extra cent that you have put it towards getting rid of this debt!

Once that debt is gone you have the minimum payment (plus all those extra pennies) to add to the minimum monthly payment of debt #2. Continue working your way through all of your debts, throwing as much as possible at a single debt at a time. Make sure you make all minimum monthly payments on your other debts as you work through your list.

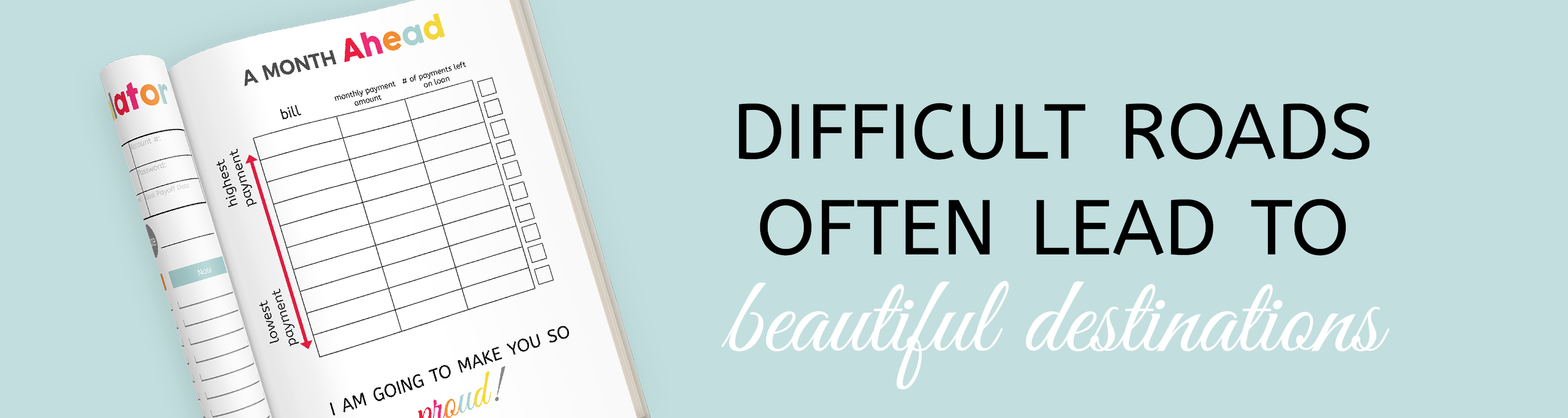

A month ahead

If you have more than $50,000 in debts (and cannot get them knocked out completely within 2 years) I recommend that you work towards getting a month ahead on your payments – this helps to cover any emergencies – mistakes (whoops! I got sick, and missed my payment date), etc. This keeps your credit score safe as you work on paying off our debts – so what when they are finally gone, you are in excellent financial health!

Financial Breakdown

At the start of every month go through the questions in a row and answer them. Here you will be able to see your savings climb, your debts decrease, and hopefully your income increase (as you increase your irregular income)

Monthly Budget Check-In

At the end of each month sit down (if you are married, sit down with your spouse) and do a check-in to go over how your budget went for the month – and to prepare for he next one!

Phew! This post is a big one – but I am so happy to have walked your through all the pages. If you have any questions at all please do not hesitate to send me an e-mail! [email protected]

wow, it looks awesome and very organized. I have told many friends about this 2017 Planner. I just order mine and will write in my stuff so that

when January 1, 2017 comes. I will be already in the swing of working my goal.

I plan to have by 2017 Planner printed out a Staples and Bonded into a book. I will additional stuff to it as well that are useful to my specific goals.

Thanks,

Hello! This is the second year I have used your financial planner and it just gets better! I was wondering…do you explain anywhere about the envelopes included? I have them all ready but wasn’t sure how to utilize all the check boxes on the front of them.