Today I want to give you a little insight into the world of minimum payments. What I am about to say to you does not apply to loans from a bank (For a mortgage, a car, or a home improvement loan). Today, I am referring to credit cards, student loans, and payday loans).

Based on my personal experience (I’ll show you below) the minimum payment that is due for our student loans was calculated to 1) pay the interest on our loan, first) and 2) keep us there for as long as legally possible.

Throughout this post I am going to be using a single student loan as an example. We have 4 through MyGreatLakes, and what seems like a billion through Navient (Formally Sallie Mae). I will be using just one from MyGreatLakes… Buckle Up- Here we go …

We started paying on this loan back in June of 2013. So far we have made 31 monthly payments. We pay MyGreatLakes 300.00 a month, which ends up being 73.00 towards this one loan. Here are some Facts:

- This is not our snowball account (we are working on Navient, right now.) However I pay 13.00 more than the minimum payment – every.single.month JUST so it is a nice round number (300.00)

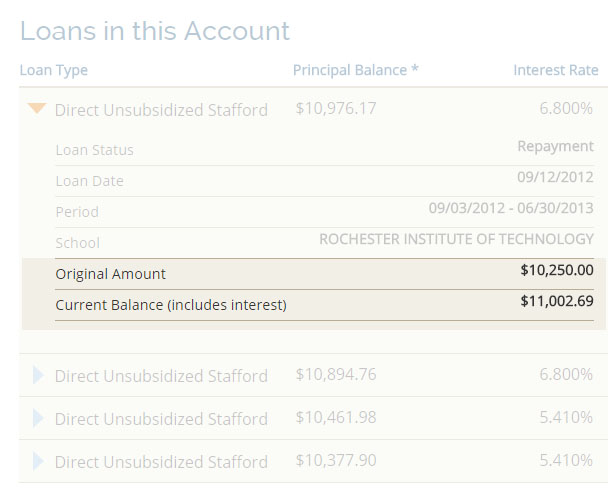

- This one loans (remember we have FOUR of them) starting balance was $10,250.00

- We have never missed a payment – never late …

- Our current balance due is – $11,002.69

- YEP! We currently owe $752.69 MORE than when we started 31 months ago!

- Those 31 months we have paid 2,325 towards this single loan (That does not seem like much, but when our total student loan debt repayment is over 1,300 a month) and we owe MORE than when we started.

Here are some hard hitting truths about minimum payments:

- This loan is setup to last 25 years, however after 24 years they will be kind enough to “forgive” the remaining balance

- Out of fear that a person will go as hard as they can at paying down their debts, they apply the majority of your payment to interest for the first decade or so, so they can be sure to get as much as possible

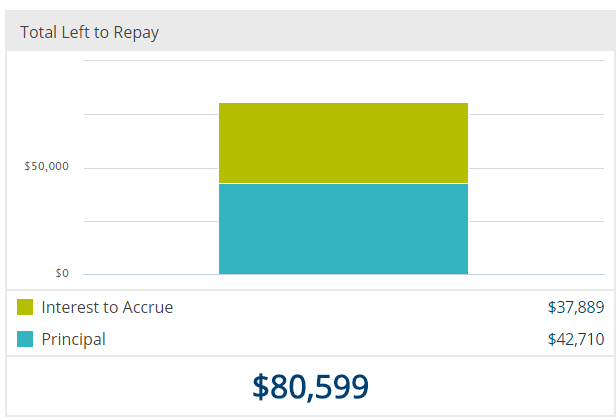

- IF we did not try to pay down our student loans as fast as possible, but instead just paid the minimum balance due every month we (us personally) would end up spending the following:

- $80,599 on a $42,710 loan!

- $37,889 on interest

Just Paying you Minimum Payments:

Did you know that the same companies who SET your minimum payments due – can also “ding” you for just paying the minimum amount due. If you ever needed to extend your credit, due to an emergency…. even if you have spent years paying the minimum payment due, always paying on time – they might not give you any additional credit because according to them, they’d would have liked to see you pay MORE than the minimum payment.

This might be a huge blessing in your life – since I do not want any of you taking more loans out, but I am also aware that emergencies do happen.

What can I do about it?

I get asked this question a lot. ‘What can I do about it?” I know a lot of people feel like they are barely getting by. They have student loan debt like us, or they have credit card balances through the roof (Or maybe both!)

The truth is, there is a lot you can do. It will be a lot of hard work, and some serious sacrifice, BUT you can absolutely become debt free!

- Get started, today. Grab the Debt Free Workbook, and stop wasting time!

- In all seriousness, I know that you can pay down a 40,000 loan in two years, one if you work really really hard!

- Make More Money – It sounds easier said than done – but it is not! Your options are endless.

- Meal Plan! – STOP wasting money at the grocery store, and STOP throwing your money in the garbage via rotten

And I want to help you!! I have been working behind the scenes to create an affordable E-Course that goes along with (and way beyond) my Soon-To-Be Debt Free Workbook! This E-Course is designed for people who are serious about attacking their debts – so they can live a debt free lifestyle!!

It will be launching soon – and I am really excited to tell you guys all about it as soon as we are ready!

Leave a Reply